Categories

real estate market 2026, RentingPublished March 13, 2026

Is the American Dream Dead? Buying vs. Renting in Rochester, NY: Building wealth in the Modern Economy - Part 1

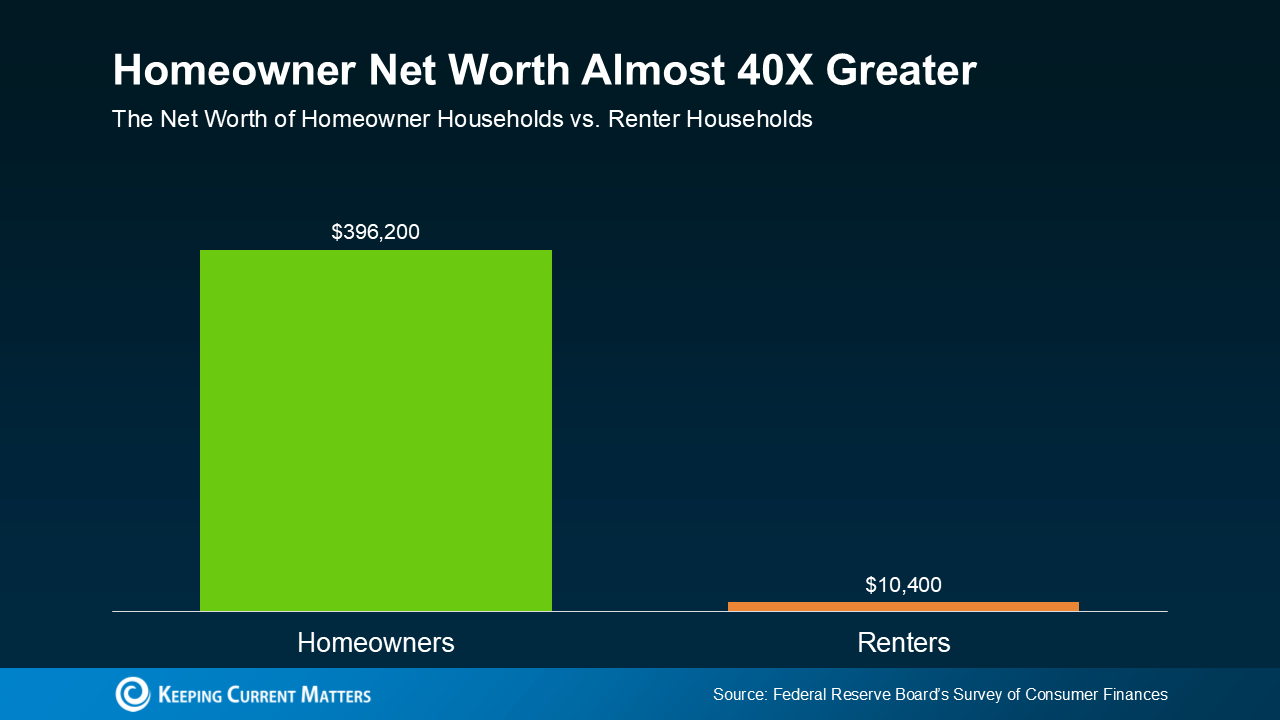

How Homeownership Builds Wealth Over Time

That 30 to 50 times wealth gap can sound dramatic at first. The reality behind it is much simpler. It usually comes down to how housing works over time.

Let’s break it down into four reasons:

#1: Forced Savings

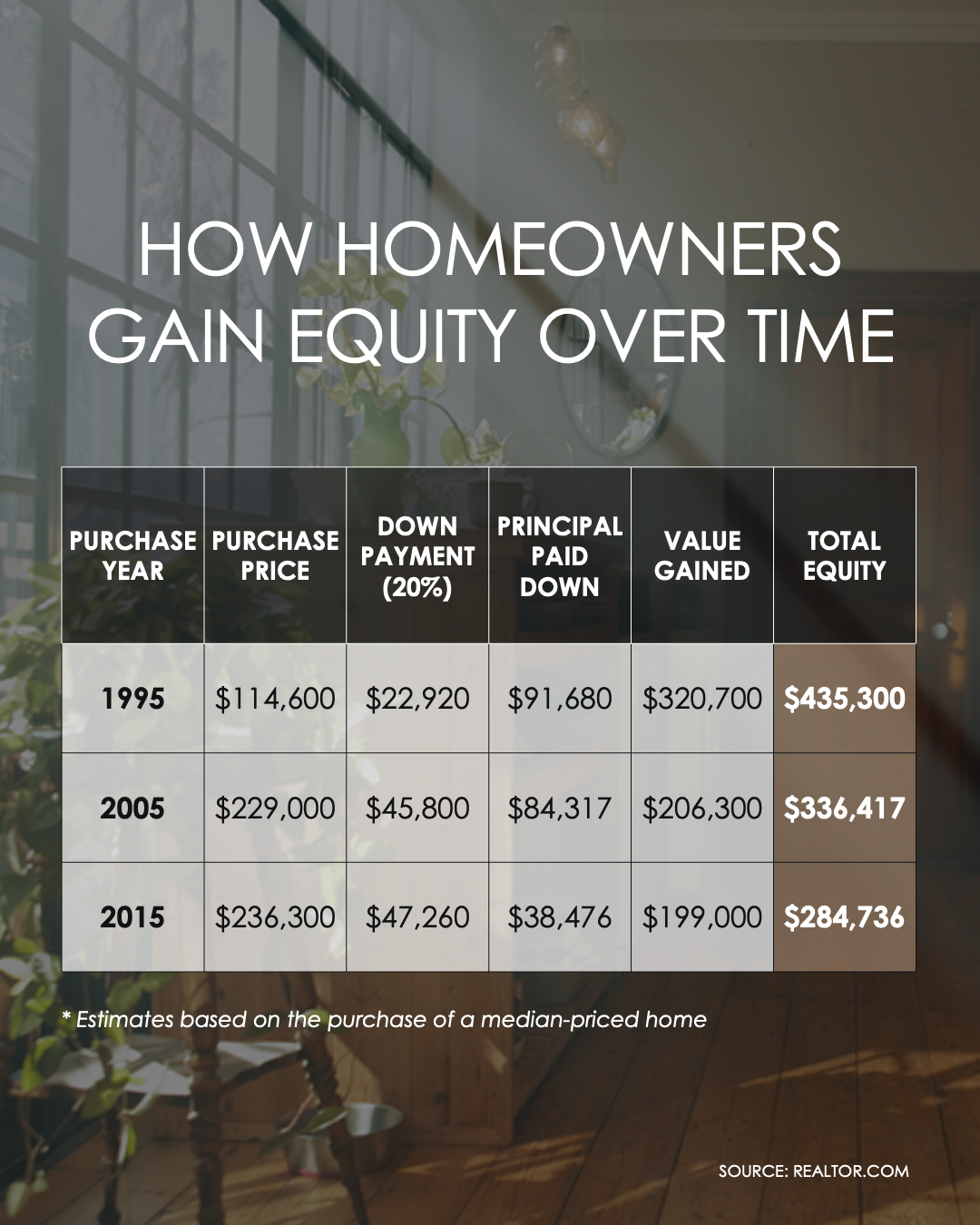

When you make a mortgage payment each month, part of that payment reduces the loan balance. In other words, you are slowly turning monthly housing costs into ownership.

Over the years, those principal payments build equity in the property.

Rent payments serve a different purpose. They cover the cost of housing for that month, but they don’t create an ownership stake in the property.

#2: Appreciation

Real estate values tend to rise over long periods of time. The increases aren’t always steady from year to year, but many homeowners see meaningful gains simply from holding the property for a number of years.

#3: Leverage

When you buy a home, you control a large asset with a relatively small down payment. If the value of the home rises, the gain applies to the full property value.

That dynamic can accelerate wealth growth compared with saving the same amount in smaller increments.

#4: Long-term Ownership

Equity builds slowly through loan paydown and price growth. The longer someone owns their home, the more time those forces have to accumulate.

Over a decade or two, the results can become significant.

This combination of forced savings, appreciation, leverage, and time helps explain why homeownership has remained one of the most consistent ways households build wealth over the long run.

The Timing Effect: Why Buying Earlier Can Make a Big Difference

Once you understand how equity builds, another factor becomes clear: the age when someone buys their first home can shape how much wealth they accumulate later in life.

In fact, households that buy a home by age 30 tend to have 22.5% higher net worth by age 50, which works out to about $119,000 more wealth than households that wait until their 40s to buy.

That difference usually comes down to how long the home has to build equity.

When you buy earlier, you give yourself more years for property values to rise and for mortgage payments to reduce the loan balance. Over time, those two forces add up to a significant advantage.

The report breaks the effect down further.

- Buying between ages 28 and 32 is associated with about 22.5% more net worth by age 50, or roughly $119,000 more wealth

- Buying between ages 33 and 37 is linked to about 11.2% more net worth, or about $59,000 more

- Buying between ages 38 and 42 shows a smaller difference of about 1.5%, or roughly $8,000

Most homeowners don’t notice these changes month to month. They tend to show up gradually over years of ownership as equity builds and home values change.

Buying earlier simply means giving that process more time to unfold.

Article Source: Realtor.com, BAM, Federal Reserve, Keeping Current Matters

|

or another way